Unlocking the Secrets of AARP Plan F: Navigating Benefits and Costs

Are you seeking a sense of serenity when it comes to your healthcare expenses in retirement? Navigating the complex world of supplemental insurance can feel overwhelming, but understanding the nuances of AARP Plan F can bring a sense of calm and clarity. Let's embark on a journey to unravel the tapestry of benefits and costs associated with this popular Medigap plan.

Imagine a world where unexpected medical bills don't disrupt your financial equilibrium. AARP Plan F, offered by UnitedHealthcare, is designed to supplement Original Medicare (Parts A and B), potentially minimizing your out-of-pocket expenses. This comprehensive coverage can offer peace of mind, allowing you to focus on enjoying your retirement years.

AARP Plan F, a Medigap policy, was established as part of the standardized Medigap plans outlined in federal law. It's crucial to understand that the plan's core purpose is to help cover the "gaps" in Original Medicare, such as co-pays, coinsurance, and deductibles. This structure can be especially appealing to those seeking predictable healthcare costs.

A significant concern for many retirees is the rising cost of healthcare. Evaluating the financial implications of AARP Plan F is paramount. While the plan offers comprehensive coverage, it's essential to weigh the monthly premiums against the potential savings on medical expenses. This careful assessment requires considering your individual health needs and financial situation.

One of the most crucial aspects to grasp about AARP Plan F is that it's no longer available to those new to Medicare after January 1, 2020. Existing enrollees can continue their coverage, but those newly eligible for Medicare will need to explore alternative Medigap options, such as Plan G or Plan N. This change highlights the dynamic nature of healthcare policies and the importance of staying informed.

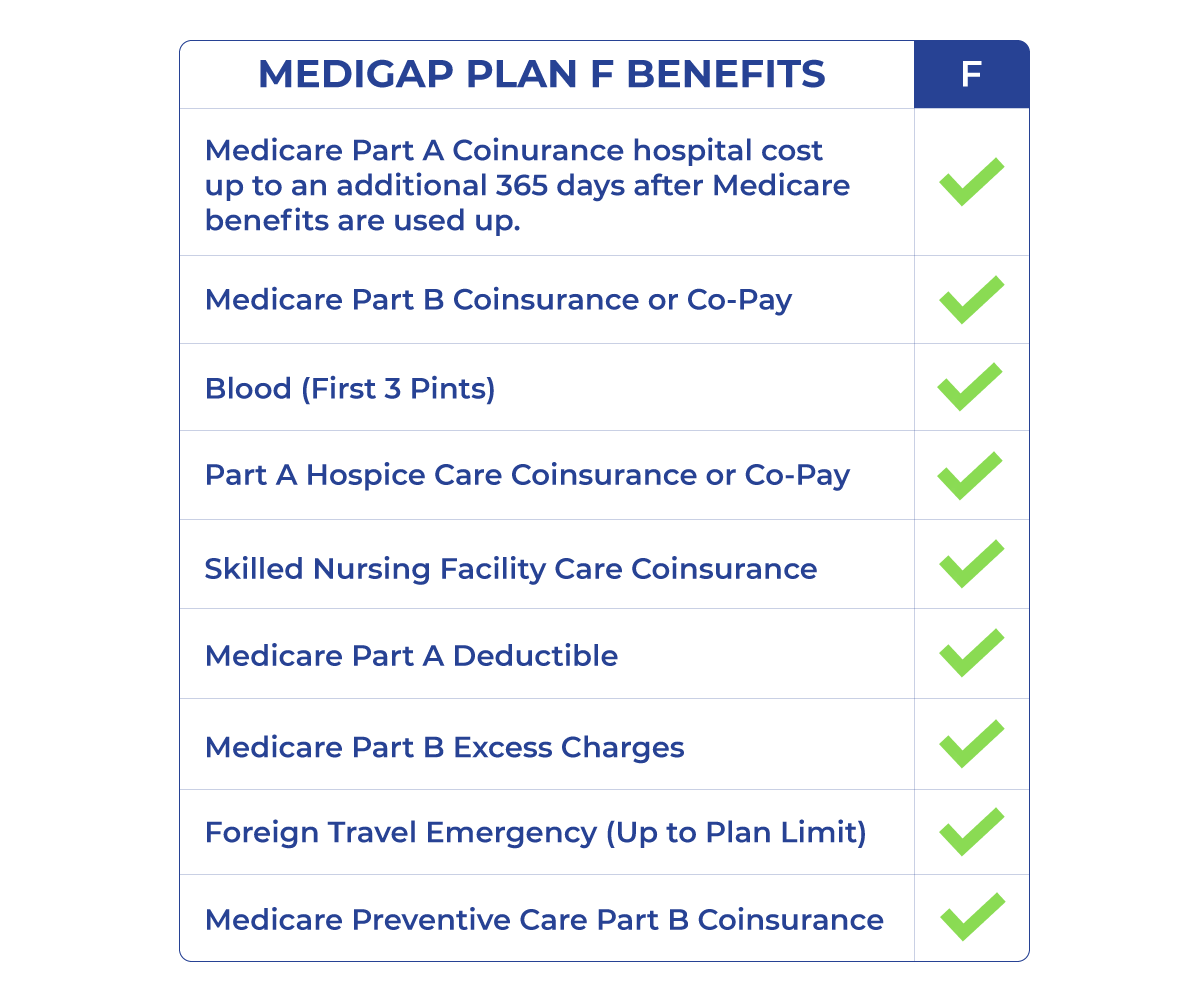

AARP Plan F helps cover Medicare Part A and Part B coinsurance, copayments, and deductibles. For example, if you have a hospital stay, Plan F might cover the Part A coinsurance. It also covers the Part B deductible and coinsurance for doctor visits and other outpatient services.

Benefit 1: Predictable Costs. Knowing your out-of-pocket expenses are largely covered can bring financial stability. Example: A retiree with Plan F can budget for their monthly premium knowing they'll have minimal additional expenses for covered services.

Benefit 2: Comprehensive Coverage. Plan F offers the most comprehensive coverage among Medigap plans (for those eligible). Example: AARP Plan F covers the Part B deductible, which other plans may not.

Benefit 3: Travel Coverage. Plan F covers medically necessary emergency care abroad (subject to certain limitations). Example: If you become ill while traveling, Plan F can help cover eligible expenses.

If you're considering AARP Plan F (and are eligible), compare quotes from different insurance companies offering the plan, factor in your health needs and budget, and consult with a licensed insurance agent or financial advisor to discuss your options.

Advantages and Disadvantages of AARP Plan F

| Advantages | Disadvantages |

|---|---|

| Predictable Costs | Higher Premiums |

| Comprehensive Coverage | Not Available to New Medicare Beneficiaries |

| Foreign Travel Emergency Coverage | May not be the most cost-effective option for everyone |

Best Practices: 1. Compare Plans: Don't settle for the first plan you see. 2. Review Your Needs: Consider your health status. 3. Budget Wisely: Factor in the premiums. 4. Understand the Coverage: Read the fine print. 5. Seek Professional Advice: Talk to a financial advisor.

FAQs: 1. What does AARP Plan F cover? (Answer: Medicare cost-sharing). 2. How much does it cost? (Answer: Varies by location and insurer). 3. Who is eligible? (Answer: Those who were eligible for Medicare before 2020). 4. Is it worth it? (Answer: Depends on individual needs). 5. What are the alternatives? (Answer: Plan G, Plan N). 6. Can I switch plans? (Answer: Possibly, depending on circumstances). 7. Where can I get more information? (Answer: Medicare.gov, UnitedHealthcare). 8. What is the difference between AARP and UnitedHealthcare? (Answer: AARP endorses the plans offered by UnitedHealthcare).

Tip: Shop around for the best premium rates. Trick: Consider your expected healthcare usage when choosing a plan.

In conclusion, navigating the landscape of supplemental Medicare insurance requires careful consideration. AARP Plan F, with its comprehensive coverage, offered peace of mind to many, but its unavailability to new Medicare beneficiaries underscores the evolving nature of healthcare options. By diligently evaluating your individual needs, comparing plans, and seeking expert guidance, you can empower yourself to make informed decisions that align with your financial and health goals. Take the time to explore your options, ask questions, and prioritize your well-being as you navigate this important stage of life. Understanding the interplay of benefits and costs is paramount to securing a healthy and financially secure future. Reach out to a licensed insurance agent specializing in Medicare to personalize your approach and ensure you have the right coverage for your unique circumstances.

Unveiling the exquisite world of plantation rum panama 27 years

Unlocking bass wiring three dual voice coil subwoofers

Flamingo resort costa rica a sun kissed escape